Stocks soared, as long-term interest rates rose, but housing reports next week could show weakness in that sector.

The Week That Was

November Consumer Price Index (CPI) data show the total CPI up at a 1 percent annual rate for each of the past two months. Core CPI, which excludes food and energy, remained above 3 percent for the last two months. The year-over-year rate remains at 4 percent. While inflation down, it’s too soon to take a victory lap.

November retail sales rose at a 3.5 percent annual rate. This is consistent with a similar slowdown in income data. Look for a further slowing in sales in the months ahead due to the delayed impact of monetary restraint.

Weekly unemployment data continue to point to low rates of unemployment claims and only a slight rise in unemployment payments going into the first week of December. These data show no signs of any significant weakening in the economy.

Today’s S&P flash business survey for early December shows the service sector continuing to grow, albeit at a subdued pace. The survey also shows inflationary pressures remain a problem.

Things to Come

On Monday, Homebuilders will report on their latest assessment of new housing conditions. The November Index was deep in negative territory at 34. The sharp decline in interest rate in December will improve conditions. However, we project housing conditions will remain negative with a reading below 50.

Additional housing data later in the week should continue to show an ongoing weakness in permits, starts and housing sales.

Friday, the November report on consumer spending and incomes will provide the most complete view of the economy. It also will provide another view of inflation. Expect these data to continue to show spending and incomes growing at a 3 percent to 4 percent annual rate, down from the 5 percent to 6 percent rates of the prior six months.

Market Forces

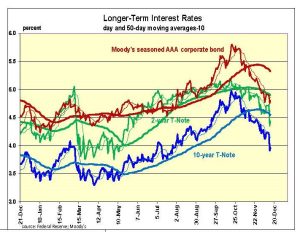

Powell warned against assuming inflation was down. He even warned of the need to raise interest rates further if inflation remains above the Fed’s target. To back it up, the Fed is continuing to sell securities. This means policies will become more restrictive, at least through January.

Pay attention to what the Fed does, not to its forecast of interest rates. Do not be stampeded by what the herd on the street are saying.

The Fed does not expect inflation to reach its 2 percent target until 2026. Thus, the market’s expectation of the Fed is signaling rate cuts is inconsistent with the Fed’s own inflation forecast.

Outlook

Economic Fundamentals: positive

Stock Valuation: S&P 500 overvalued by 20 percent

Monetary Policy: restrictive

For more analyses by Robert Genetski.

For more great content from Budget & Tax News.

For more from The Heartland Institute.