Robert Genetski: Inflation and interest rates moving lower, stocks continue their upward trend. (Commentary)

The Week That Was

The June CPI report showed inflation was below even the Cleveland Fed’s low estimate. The total monthly index was down 0.06 percent and core inflation CPI was 0.06 percent higher. Year-over-year rates were 3.0 percent for the total and 3.3 percent for core inflation.

Recent inflation news has benefited from a sharp decline in oil and energy prices in May and June. However, July’s oil prices are up 3 percent from June, a 40 percent annualized rate. As such, next month’s inflation report will be less encouraging.

Nothing in the weekly unemployment data point to any meaningful change. Initial unemployment claims were down sharply in the first week in July. Those receiving insured unemployment payments were up, but only slightly in the most recent week.

Things to Come

Tuesday’s retail sales report should be informative. Retail sales have been among the weakest (and least reliable) of the monthly indicators. They show annualized gains at only a 2 percent rate in recent months, as well as over the past year.

With personal incomes and wages and salaries increasing at 4 percent to 5 percent annual rates, at some point retail sales should experience a significant pickup. There is no telling if this occurred in June. Available information on oil prices and vehicle sales in June show continued signs of weakness. This suggests the retail sales slump may have continued.

Also on Tuesday, the Homebuilders report their Index for early July. For the past two months, the Index fell below breakeven of 50. With mortgage rates staying in the 7 percent vicinity, look for housing Index to remain below 50.

Wednesday there will be more housing data for permits and starts. These are likely to show a depressed housing market.

Market Forces

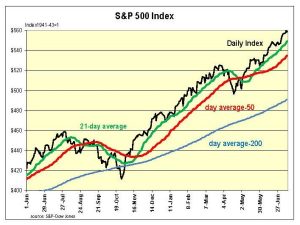

Like the Little Engine that Could, stocks continue to move still higher. The S&P500, Nasdaq and QQQs [funds that track the Nasdaq-100 Index™] all surged to new all-time highs before yesterday’s slight reversal.

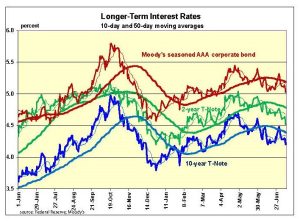

This week’s main news was yesterday’s better than expected inflation report. It caused interest rates to drop immediately. Financial markets now place the odds at 88 percent that at their September meeting the Fed will cut their target rate to from 5.33 percent to 5.13 percent.

According to the Atlanta Fed model the economy grew by 2.0 percent in the second quarter. As we enter the third quarter, economic numbers remain mixed, buy offer little guidance to any major changes.

Outlook

Economic Fundamentals: positive

Stock Valuation: S&P 500 overvalued by 36 percent

Monetary Policy: restrictive

For more analyses by Robert Genetski.

For more great content from Budget & Tax News.

For more from The Heartland Institute.