Robert Genetski: Declining stock prices, rising unemployment make September interest rate cut almost certain. (Analysis)

The Week That Was

Today’s jobs report shows the July unemployment rate rose to 4.3 percent. As in prior reports, there has been no significant increase in jobs over the past year from one survey, while an alternative measure finds a modest 114,000 new jobs

With the government’s job data providing widely differing trends, a better measure is the ADP data based on 132 million payrolls. The July numbers show private job gains of 122,000, a 1 percent annualized increase. This is down from a 1.4 percent rate over the past year.

Yesterday’s July manufacturing surveys show a general weakness. The July ISM survey, which has consistently showed negative activity for the past year, reported an overall score of 47 (50 is breakeven). The alternative S&P manufacturing survey, moved slightly below 50.

The Fed meeting was mostly uneventful. While keeping its target rate unchanged, the Fed continued plans to sell $40 billion in securities each month. Security sales tighten monetary policy, a move that is inconsistent with lowering interest rates.

Things to Come

The only significant reports this coming week are service company July business surveys. S&P service sector advanced estimate for early July pointed to a booming service sector early in July. We expect the S&P survey for the whole month will be strong.

In contrast, the ISM June service sector survey dipped below breakeven. Given the size of the service sector, the ISM report signaled a downturn in the overall economy.

Financial markets tend to place more weight on the ISM surveys. As a result, another negative month should send interest rates lower. If the survey were to rebound, it would put some mild upward pressure on rates.

Market Forces

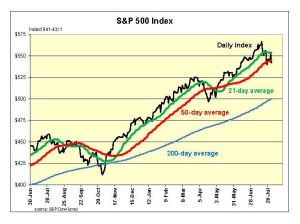

This week an erratic stock market ended with most indexes down about 1 percent. The S&P500 soared on Wednesday from it 50-day average to its 21-day average, before returning to its 50-day average.

Ironically, reported profits (which analysts often ignore) were much better. They were 10 percent from the first quarter and 7 percent above a year ago.

With no significant economic news, the Fed kept its target rate unchanged. However, Powell said he expected a rate cut to be discussed in September. However, the Fed’s decision would depend on the data driven. Hence, nothing has changed.

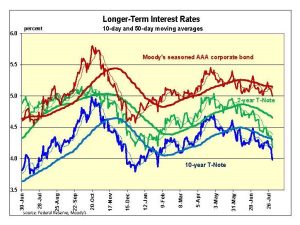

Futures markets place the probability at 80 percent for a ¼ percent rate cut and 20 percent for a ½ percent cut. The 5.1 percent yield on the 6-month T-bill bill shows the yield curve also expects a cut, but at a slower pace.

Our momentum model shows a 60 percent probability of an upward trend in the S&P500. This is not a favorable environment for stocks, particularly with the S&P500 remaining 32 percent overvalued. Moreover, if stocks move convincingly below the 50-day average (as indicated by this morning’s futures markets) the odds of a further decline in stocks will increase considerably.

Outlook

Economic Fundamentals: neutral

Stock Valuation: S&P 500 overvalued by 33 percent

Monetary Policy: restrictive

For more analyses by Robert Genetski.

For more great content from Budget & Tax News.

For more from The Heartland Institute.