By Richard M. Salsman

Worries have intensified and spread lately about the prospects of higher U.S. inflation in the coming years. It’s an important issue because higher inflation, even if it remains in the “single digits,” erodes the value of financial assets (bills, bonds, and stocks) relative to tangibles (precious metals, other commodities, real estate). Double-digit inflation inflicts still worse harm, as it also sabotages economic growth and boosts the jobless rate (the “stagflation” combination of the 1970s).

Is there evidence today of forthcoming higher inflation in the U.S.? By some accounts, yes. U.S. inflation expectations today are worse than at any time since 2011 according to the “TIPS spread” (the difference between nominal Treasury note yields and the real yield on Treasury Inflation-Protected Securities). The spread has widened over the past year and is now 2.5% points. However, two other reliable market-based signals suggest inflation will stay low. The U.S. dollar has appreciated by 3% in foreign exchange this year, after depreciating by 7% in 2020; the $/gold price also is down, by 11% so far this year, after rising 28% in 2020. In short, predictive market prices are not signaling a materially higher inflation rate in the U.S.; as it is, the CPI rate itself has decelerated steadily over the past year, to only 1.4% (down from 2.5% over the prior-year period).

Of course, the Federal Reserve lately has massively increased bank reserves and the money supply in the process of recklessly monetizing a U.S. national debt that now totals $27 trillion (double its level of a decade ago). Bank reserves are now $3.4 trillion, double the level of a year ago (a magnitude not seen since the 2008-09 crisis). Significantly, most of these are excess reserves (beyond those required by the Fed), which means banks are hoarding cash. Indeed, they’ve been doing so since 2008-09. Likewise, the money supply (M-1) has increased substantially over the past year (+350%), to $18.4 trillion, although most of that occurred in 2Q2020. But the demand for money (cash balances) also has risen a lot, which means money’s velocity (rate of speed in spending) has been plummeting. Whereas velocity is the multiple of nominal GDP to the money supply, money demand is the inverse (the multiple of money supply to nominal GDP, or the reciprocal of velocity). Fast-rising money demand (fast-declining velocity) signifies hoarding.

Banks, businesses, and households tend not to hoard money in good times, or when they have confidence in the credibility and predictability of policymakers; they hoard in bad times, when they lack sufficient confidence. That is precisely the case today, even if officials won’t admit it.

We should always remember that the value of money (its purchasing power) is determined – like the value of other goods – by supply and demand, never by supply alone. Consider three separate occasions since the turn of the century (2001-02, 2008-09, and 2020-21) when faulty inflation forecasters failed to consider both factors. Yes, in each episode, out of sheer panic, the Fed massively increased reserves and money (supply), but banks, businesses, and households likewise massively increased their holdings of idle cash (demand for money). This helps explain why the dollar’s value has not (yet) plunged despite these massive increases in Fed money creation.

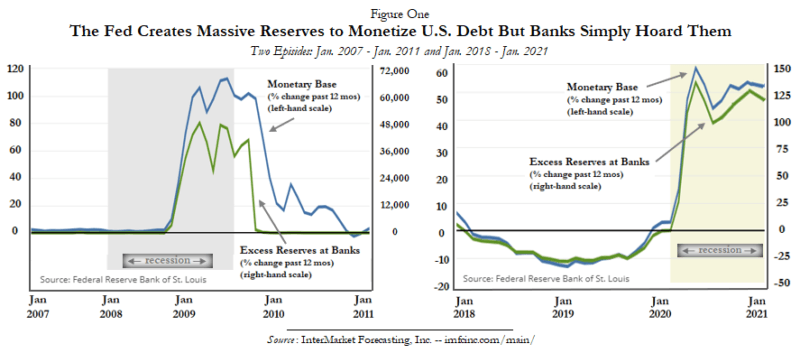

Figure One illustrates the last two episodes of massive creation of bank reserves by the Fed. Notice how the banks mostly held onto those reserves, which far exceed the sums they are required (by the Fed) to hold against deposits. This must be part of any account of inflation remaining low. Of course, the Fed could claim prescience and insist that it created these reserves precisely because it foresaw the banks would need them badly and hold them dearly. That is just false. The Fed hoped to stem panic, spur lending, and “stimulate” the economy. Mere money creation cannot do that.

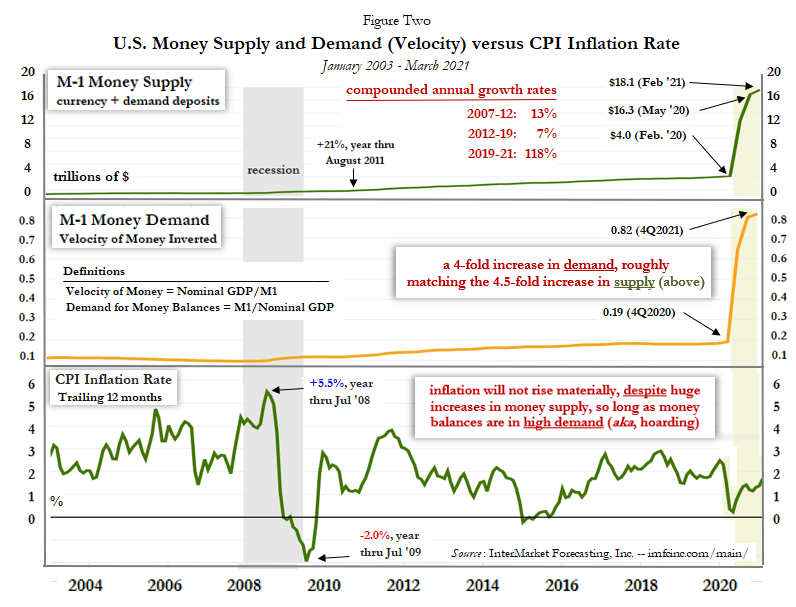

Figure Two illustrates the vast increases in both U.S. money supply and money demand over the past year, compared to other years since 2004. It also shows that the CPI inflation rate certainly has not skyrocketed – because money demand has risen roughly as much as money supply.

The laws of economics have not been repealed, although acolytes of “MMT” (Modern Monetary Theory) like to hope so; they want money and debt alone to cheaply fund stupendous increases in public spending – including a “universal basic income guarantee” and the “Green New Deal” – without their favored politicians suffering electoral fallout from much-hated tax-hiking schemes. The fans of MMT neglect the demand for money (and debt); the best-laid plans of mice-like men come to naught. A hoarding nation is rarely a prosperous one, and government can rarely secure real resources from a stagnant economy; it only risks hyperinflation and/or national insolvency.

Confusion and ambiguity concerning the relationship between money supply and money depreciation (inflation) can be traced to the influence of Nobel laureate Milton Friedman and the American monetarists. They were quite right (relative to Keynesians) to contend that “inflation is everywhere and always a monetary phenomenon” (i.e., not due to real factors, like the economic growth rate or jobless rate). But for decades monetarists also falsely asserted that the demand for money was nearly constant (or changed only negligibly) and thus that money supply alone (or substantially) determined inflation. In recent decades this one-eyed view of the determinants of money’s value has led many economists and forecasters astray (especially the monetarists).

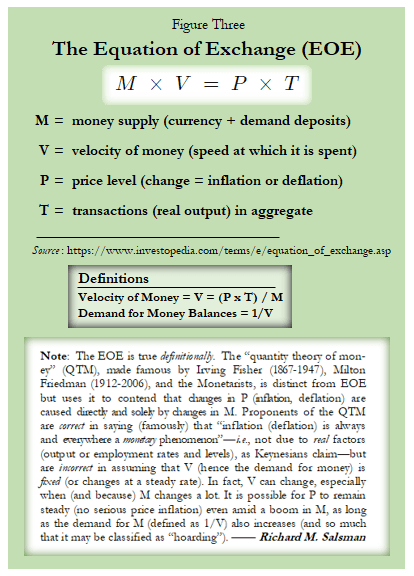

Again, the laws of economics have not been suspended; those laws include the law of supply and demand, which includes the supply and demand for money. Nor has the monetary “equation of exchange” become obsolete, as disciples of MMT also assume (for elaboration, see Figure Three).

I’ll conclude with a longer-term view of the matter. I have mentioned already the three occasions since this century began when the Fed felt it necessary to massively increase bank reserves and the money supply (2001-02, 2008-09, and 2020-21). How does its policy over the last two decades contrast with its policy over the prior two decades (1980s and 1990s)?

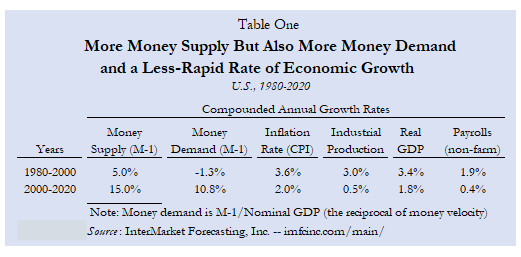

In Table One I calculate compounded annual growth rates in money supply, money demand, the CPI, real output, and jobs over the past four decades. The money supply grew by only 5.0% p.a. in the last two decades of the 20th century, versus 15.0% p.a. over the first two decades of the 21st century. Yet inflation has been much lower over the last two decades (2.0% p.a.) than it was over prior two decades (3.6% p.a.). Why? Money demand has grown a lot since 2000 (+10.8% p.a.), whereas it declined (i.e., velocity quickened) in the two decades before 2000 (by -1.3% p.a.).

Observe also: the most robust economic growth rates occurred in the last two decades of the 20th century (3.0% p.a. for industrial production, +3.4% p.a. for real GDP), compared to growth of only 0.5% p.a. and 1.8% p.a. over the first two decades of the 21st century. Employment growth also was far better in the 1980s and 1990s (+1.9% p.a.) than in the past two decades (0.4% p.a.). You sure don’t need more money to get more wealth; indeed, too much money impedes wealth creation.

As I explained two years ago, the mere production of money isn’t the production of real wealth. Table One further confirms the point. The Fed and its MMT allies believe otherwise, of course, even though the more money and debt are created, the more economies stagnate. Ask Japan how that has worked – for many decades. Or ask Paul Krugman and the Keynesians, who’ve advised this policy for as many decades; just don’t expect an honest answer from them, because the more prolonged the stagnation they cause, the more they demand still stronger versions of their policy.

Just because a reckless central bank foists tons of fake money on banks, businesses, and households does not mean any of them must spend it. Fiscal-monetary recklessness itself can signal private-sector actors not to part with safe, liquid assets. Eventually, of course, they may choose to flee the money and the debt, bringing higher inflation rates and higher interest rates. Meantime, the prudent observer must never neglect to consult the demand side of money.

Originally published by the American Institute for Economic Research. Republished with permission under a Creative Commons Attribution 4.0 International License.

")

{kind=link}