By Robert Hughes

Sales of existing homes sank another 1.5 percent in September, to a 4.71 million seasonally adjusted annual rate. That is the eighth consecutive monthly decline leaving the selling pace at the lowest level since May 2020, the low of the lockdown recession. Excluding the lockdown recession, sales are at their lowest since September 2012. Sales were down 23.8 percent from a year ago and 27.4 percent from the January peak.

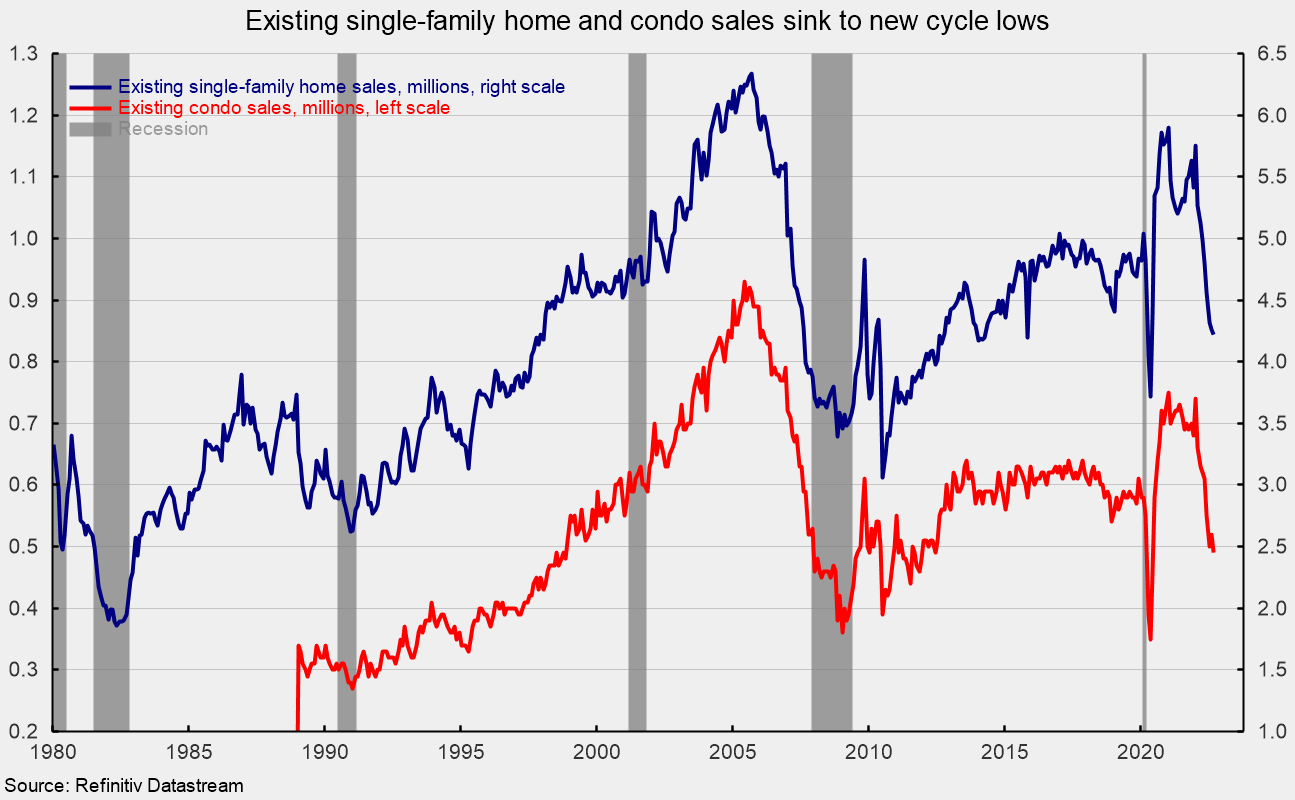

Sales in the market for existing single-family homes, which account for about 90 percent of total existing-home sales, dropped 0.9 percent in September, coming in at a 4.22 million seasonally adjusted annual rate (see first chart). Sales are down 23.0 percent from a year ago and 26.6 percent from the January peak. Single-family sales also fell for the eighth consecutive month and were at their slowest pace since the May 2020 lockdown recession.

The single-family segment saw sales decline in three of the four regions. Sales fell 1.1 percent in the South, the largest region by volume, 1.8 percent in the Midwest, and 1.9 percent in the Northeast, the smallest region by volume, but rose 1.3 percent in the West. Sales were down double-digits in all four regions from a year ago (-31.0 percent in the West, -22.2 percent in the South, -20.1 percent in the Midwest, and -17.7 percent in the Northeast).

Condo and co-op sales fell 5.8 percent for the month, leaving sales at a 490,000 annual rate for the month versus 520,000 in August (see first chart). Measured from a year ago, condo and co-op sales were off 30.0 percent, and were at their slowest pace since June 2020.

Condo and co-op sales were down in two of the four regions in September, falling 8.3 percent in the South and 9.1 percent in the West but were unchanged in the Northeast and the Midwest. From a year ago, sales were also down in all four regions (-35.3 percent in the South, -33.3 percent in the West, -23.1 percent in the Northeast, and -12.5 percent in the Midwest).

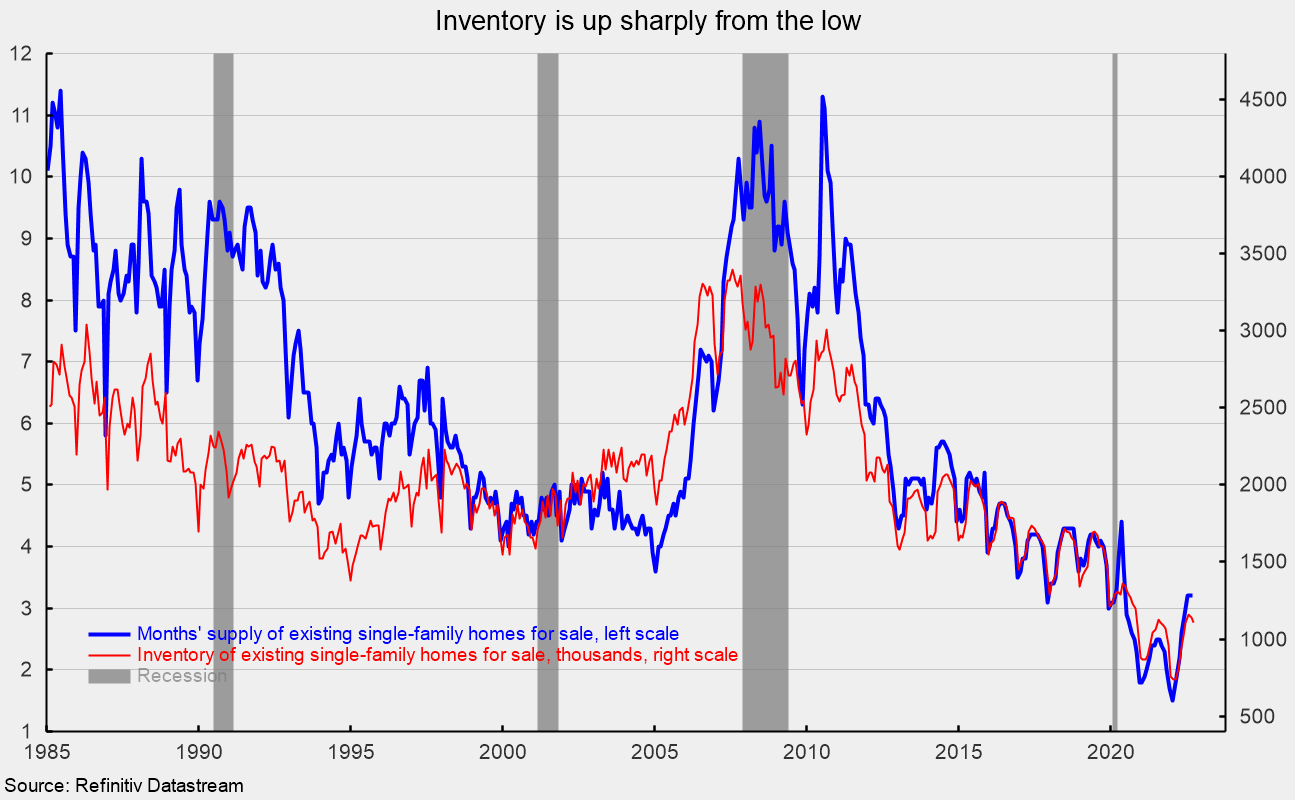

Total inventory of existing homes for sale fell in September, decreasing by 2.3 percent to 1.25 million, leaving the months’ supply (inventory times 12 divided by the annual selling rate) unchanged for the third consecutive month at 3.2, matching the highest since June 2020, but still low by historical comparison.

For the single-family segment, inventory was down 2.6 percent for the month at 1.10 million and is 1.8 percent above the September 2021 level (see second chart). The months’ supply was 3.2, unchanged from the prior month and the highest since June 2020 (see second chart). The condo and co-op inventory decreased 4.3 percent to 135,000, leaving the months’ supply at 3.3. Months’ supply is 17.9 percent above September 2021.

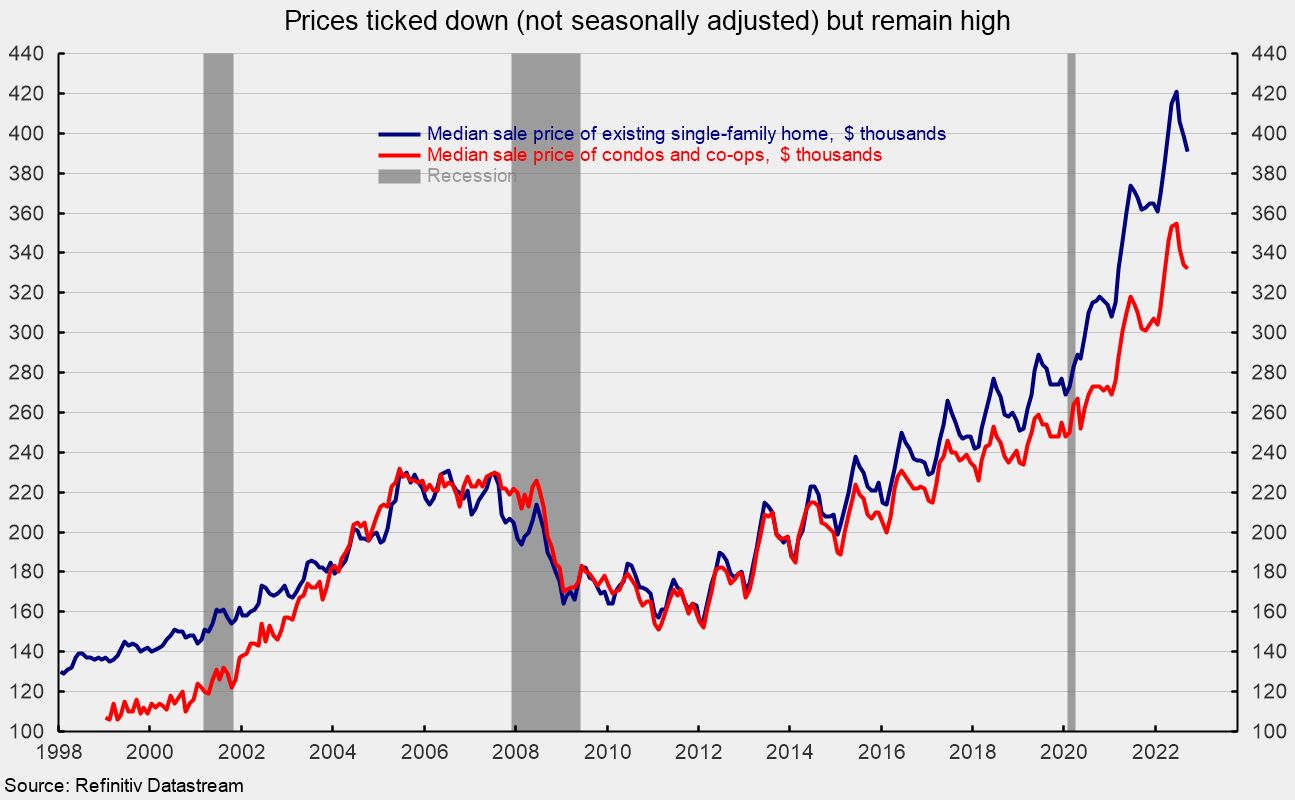

The median sale price in September of an existing home was $384,800, 8.4 percent above the year ago price. For single-family existing home sales in September, the price was $391,000, an 8.1 percent rise over the past year (see third chart). The median price for a condo/co-op was $331,700, 9.8 percent above September 2021 (see third chart).

Mortgage rates have been surging again recently, hitting 6.94 percent around mid-October, well above the lows of around 2.65 percent in January 2021 (see fourth chart).

The combination of near-record-high home prices and sharply higher mortgage rates has sent housing affordability plunging. The Housing Affordability Index from the National Association of Realtors measures whether or not a typical family could qualify for a mortgage loan on a typical home. A typical home is defined as the national median-priced, existing single-family home as calculated by NAR. The typical family is defined as one earning the median family income as reported by the U.S. Bureau of the Census. A value of 100 means that a family with the median income has exactly enough income to qualify for a mortgage on a median-priced home. An index above 100 signifies that a family earning the median income has more than enough income to qualify for a mortgage loan on a median-priced home, assuming a 20% down payment. As of August, the index stood at 104.4, slightly above the recent low of 94.5 in June, but is likely to head lower in coming updates (see fourth chart).

Housing is likely to continue to be under intense pressure as near-record-high prices and surging mortgage rates reduce affordability and push more and more buyers out of the market.

Originally published by the American Institute for Economic Research. Republished with permission under a Creative Commons Attribution 4.0 International License.

More great content from Budget & Tax News

")

{kind=link}