Employment fell 310,000 in May, unemployment increased 400,000, or from 3.3 percent to 3.7 percent, signaling economic weakness.

The Week That Was

On a positive note, Friday’s strong May payroll employment report shows private jobs and hours worked continued to grow at a strong 2 percent to 3 percent annual rate. Average hourly earnings increased at a 5½ percent rate. Weekly unemployment data are consistent with payroll data.

On the negative side, the government also has a survey of households which shows May employment fell by 310,000, unemployment increased by 400,000, and the unemployment rate rose from 3.3 percent to 3.7 percent.

The picture painted by the household survey provides the Fed a reason to pause and wait for additional data before raising rates.

Another report is the May Institute for Supply Management (ISM) survey for manufacturing. It remained weak, with an overall reading 47, slightly below breakeven of 50. New orders fell to 43 and the inflation measure was 44. Despite of declines in these measures, readings for production and employment readings were slightly above breakeven at 51.

Things to Come

Today, both the ISM and S&P report on May’s service sector performance. The service sector contributes about 60 percent to the economy’s gross domestic product (GDP) versus 12 percent for manufacturing. Hence, Monday’s results are more important than for manufacturing.

April’s service sector surveys show moderate increases overall, but strong new orders. This sector will be the last to signal a downturn in the economy, so it can remain strong while other areas of the economy continue to weaken.

Markets, Money, and Interest

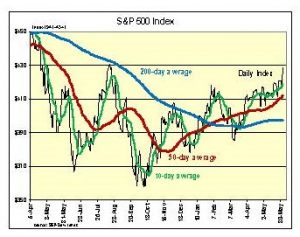

Stocks moved sharply higher this week as S&P 500 rose 2 percent, breaking though the 4,200 peak for this year. The next resistance level is 4,300.

Friday’s employment report appears to reaffirm the view that the US economy remains strong. The Atlanta Fed model continues to show the economy growing at a 2 percent rate in the second quarter.

Market, Money, and Interest

Stocks moved sharply higher last week as the S&P 500 rose 2 percent, breaking though the 4,200 peak for this year. The next resistance level is 4,300.

Friday’s employment report appears to reaffirm the view that the US economy remains strong. The Atlanta Fed model continues to show the economy growing at a 2 percent rate in the second quarter.

Monetary data for May show the money supply down 12 percent over the past year, but up 30 percent from two years ago. Hence, the Fed’s previous increase in money continues to support the economy.

In spite of the extra money, the past year’s money supply decline sent housing activity down 20 percent. It has spread through the financial system creating stress and tightening credit conditions. The stress also shows up in rail and freight shipments, which are down sharply. Despite of recent reports of growth, expect further declines in the money supply leading to a downturn later this year.

At its upcoming meeting, we expect the Fed may pause with respect to raising the fed funds rate, while still selling securities. If inflation remains high, the Fed will have little choice but to continue to raise interest rates.

The recent increase in stock prices has been on average to low volume. An improvement in technical indicators means stocks can continue to rise. However, the prospects for higher interest rates and a weaker economy are like to create problems for the market.

Outlook

Economic Fundamentals: negative

Stock Valuation: S&P 500 overvalued by 12 percent

Monetary Policy: restrictive

For more Budget & Tax News.

For more from The Heartland Institute.

")

{kind=link}