Robert Genetski: Service economy grew in July, but manufacturing is declining, and inflation remains above Fed’s goal.

The Week That Was

Most news this week shows the economy continues to grow. With the relatively strong second quarter profits, growth should continue. The S&P July survey of service companies had a strong reading of 55, along with significant strength in new orders.

The more closely watch July ISM service company survey (which was below 50 for June) moved back to 51 to 52 (positive growth) for overall activity, employment and new orders. Both surveys agree that July’s economy expanded. They disagree over the its strength.

Both surveys agree manufacturing business is declining. Since service companies represent roughly two-thirds of all output produced, the latest surveys confirm real July growth remained in the 2 percent vicinity.

Both surveys report inflation remains above the Fed’s target with upward pressure on both inputs and outputs.

Things to Come

July inflation numbers will provide the most important news this coming week. On Tuesday the government releases its estimate of producer prices. While core inflation at the producer level has slowed to 2½ percent year-over-year, the past six-month rate has been consistently in the 3 percent to 3½ percent range. Oil prices rose about 1 percent in July and commodity prices were fairly stable. Based on the business surveys noted above, we expect July monthly core producer prices increased at a 3 percent annual rate.

The Cleveland Fed estimate for Wednesday’s CPI data are 0.24 for the total and 0.27 for core. If correct the year-over-year rates remain at 3.0 percent for total and 3.3 percent for core.

With oil prices up 1 percent for the month (a 13 percent annual rate), expect the total CPI to be up more than the Fed’s estimate.

Thursday’s reports include July retail sales data. For the year ending in June, retail sales were up only 2 percent. In contrast, personal incomes and wages and salaries were up 4 percent to 5 percent. We expect the discrepancy between sales and incomes to narrow as the yearly pace of retail sales increases while gains in incomes and wages slow.

Also, on Thursday the Homebuilders’ survey for early August is expected to show a slight improvement from its depressed July level of 42. Slightly lower mortgage rates in early August should provide at least a modest boost to homebuilders’ confidence.

Market Forces

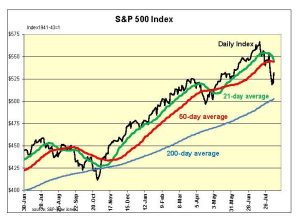

After declining by 8½ percent from all-time high in mid-July, the S&P500 rebounded yesterday. With little significant change in economic news, the recent setback could relate to political developments.

The surge in Harris’ popularity has shifted her polls and betting averages dramatically. At the same time, Trump has reminded independents why they didn’t like him. Raising issues over Harris’ race identification and calling her names is not a winning strategy. A Harris victory with soaring tax rates would be a major negative for stocks and the economy.

Technical indicators turned bearish as the S&P and Nasdaq moved well below support at their 50-day moving averages. Their 21-day averages moving below their 50-day averages is another negative sign. Our momentum model shifted to 40 percent a week ago; its 5-day average stands at 42 percent. Yesterday’s rebound brought it to 50 percent, which is neutral in terms of the stock market’s future direction.

With the S&P500 30 percent above its fundamental value and with technical indicators having a slight downward bias, conservative investors should remain defensive, at least for now.

At 4 percent, the 10-year T-Note is close to its fundamental value. Short-term rates are above their fundamental and set to begin moving down in September.

Outlook

Economic Fundamentals: neutral

Stock Valuation: S&P 500 overvalued by 30 percent

Monetary Policy: restrictive

For more analyses by Robert Genetski.

For more great content from Budget & Tax News.

For more from The Heartland Institute.

")

{kind=link}