Taxes will be a massive issue in Congress next year. Many provisions of the 2017 Tax Cuts and Jobs Act (TCJA) were temporary. Tax increases and phaseouts already began in 2022—for instance, businesses now have to spread out the costs of their domestic R&D expenses over five years rather than fully deducting these costs in the same year as incurred—and individual income tax changes expire in 2025. As lawmakers discuss the TCJA’s future, they should build on its pro-investment reforms that, overall, “helped drive economic growth, job creation, and business investment,” according to a recent report by AEI’s Kyle Pomerlau and Donald Schneider of investment bank Piper Sandler.

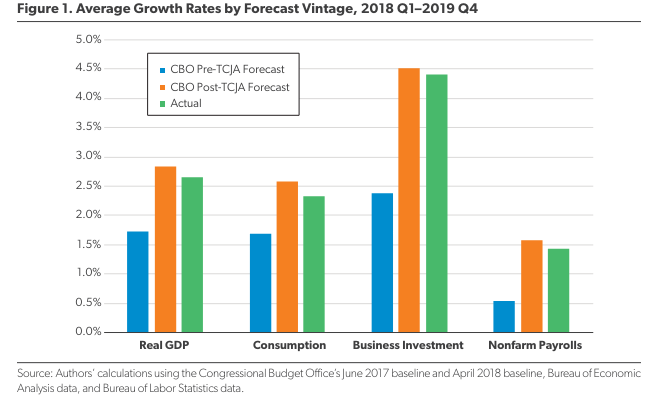

Let me highlight two charts from the report. This one shows that, after the TCJA was enacted, the actual growth rates of GDP, consumption, business investment, and nonfarm payrolls were higher than what the Congressional Budget Office (CBO) had predicted before the tax law was passed. The growth rates also aligned with the CBO’s updated projections made after the TCJA became law.

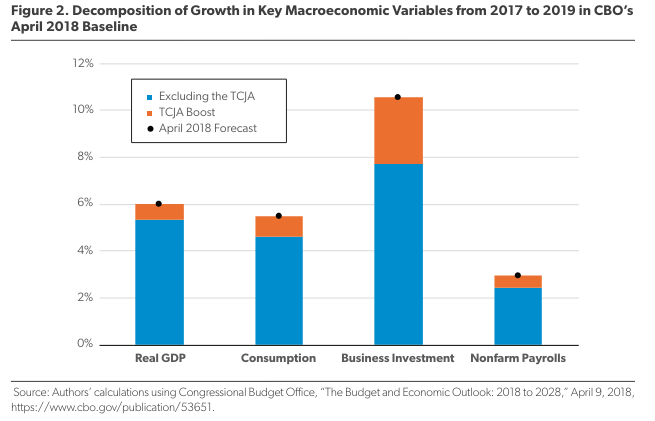

The second chart shows how much of that growth can be attributed specifically to the TCJA.

And a bit more evidence from the authors:

These macroeconomic outcomes are also consistent with microeconomic data finding that companies benefiting from TCJA increased investment. For example, according to an analysis by Gabriel Chodorow-Reich et al. using administrative data for US corporate tax returns, “the TCJA caused domestic investment of firms with the mean tax change to increase by roughly 20% relative to firms experiencing no tax change,” which is consistent with the fact that “general equilibrium long-run effects of the TCJA on the domestic and total capital of U.S. firms are around 6% and 9%, respectively.” So overall, the TCJA was positive for the economy and boosted activity in a manner consistent with CBO’s projections.

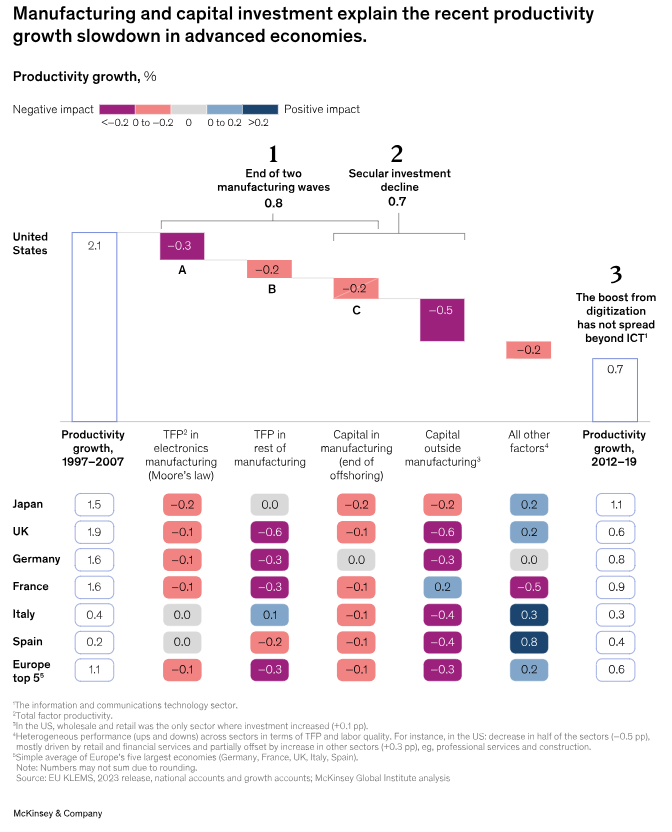

A recent McKinsey Global Institute (MGI) report, “Investing in productivity growth,” gives some broader context. The authors point out that “a marked and persistent” decline in the growth of capital per worker accounts for a significant portion of the post-Global Financial Crisis (GFC) productivity slowdown across rich economies, including the United States. For the US, specifically, MGI calculates that that decline explains half of the American economy’s post-GFC productivity slowdown to 0.7 percent from 2012 through 2019, down from 2.1 percent from 1997 through 2007. And the other half? MGI blames the “petering out” of previous manufacturing productivity gains that were driven by Moore’s Law and “the automation, restructuring, and offshoring of labor-intensive production.”

From the report:

The implications of the slowdown are significant. If the United States had not had a manufacturing slowdown, its GDP per capita in 2022 would have been around $5,000 higher. If growth in capital per worker had not declined, it would have been around $4,500 higher. Overall, if the United States had continued growing its productivity at pre-GFC rates, its GDP per capita would have been $8,900 higher in 2022. In Germany, France, and the United Kingdom, per capita income could have been $3,500 to $5,900 higher; in Japan, it could have been about $1,700 higher. Yet economies could reverse these trends in the years ahead. If they invest to regain pre-GFC productivity growth, advanced economies stand to gain between $1,500 (Japan) and $8,000 (United States) in incremental GDP per capita by 2030.

So policymakers should be thinking hard about how to boost business investment. Pomerlau and Schneider offer two possible paths forward:

The first option extends most features of the TCJA’s individual and business provisions while making incremental reforms to the tax code. It would improve on the TCJA by reducing the cost of capital and mitigating distortions and complexities while maintaining revenue neutrality. The second option is more aggressive and builds on the structure of the TCJA by enacting significant pro-growth reforms. It would reduce tax rates for individuals, broaden the tax base, and replace business taxation with a tax on business cash flow. For more details: “Making the Tax Cuts and Jobs Act Permanent: Two Revenue-Neutral, Pro-Growth Options for Tax Reform.” Let’s hope Washington doesn’t let this pro-growth opportunity go to waste.

Originally published by the American Enterprise Institute. Republished with permission.

For more from Budget & Tax News.

For more public policy from The Heartland Institute.

")

were temporary. Tax increases and phaseouts already began in 2022.){kind=link}