Mostly peaceful Trump supporters attack the capital. COVID deaths soar. Bitcoin rockets higher. Congress moves to impeach former president Donald Trump. Social media moves to censor non-woke views. The new year seems to be trying to outdo last year’s disruptive events.

Despite these unsettling developments, the near-term outlook for the economy remains positive. Unfortunately, the longer-term outlook is significantly worse.

The Democrats’ policy agenda is clear. They won the election, and they will adopt their policies. This means vast new increases in government spending and regulations, an increase in the federal minimum wage, and if they are still in charge when inflation emerges, the return of price controls.

As we prepare for the dire outcomes of these policies, our challenge as individuals is to stay with the positive trends as long as possible and adjust to the negative long-term implications before they become obvious to financial markets. We should also support organizations that are trying to inform the public about the Left’s policy agenda and how it will affect them. (Such as The Heartland Institute, publisher of Heartland Daily News.)

The economy and earnings are both growing at a rapid pace, and new orders are rising. The upward momentum is the result of a highly expansive monetary policy at the Federal Reserve, a favorable tax policy implemented by President Trump and the Republicans four years ago, and massive increases in federal spending. Increases in federal spending provide an immediate stimulus as the dollars hit the economy. Within six to nine months, however, the stimulus spending then has a depressing impact on the economy.

The massive creation of money has help bolster the economy and stock market amid government-mandated lockdowns. Money can temporarily keep the economy operating. As with spending, it’s a short-term fix with negative longer-term implications.

Employment growth has lagged the rest of the economy in the current rebound. Much of the weakness in employment is in the leisure and hospitality industries. The virus has hit these industries hard. In addition, government programs that pay people more than they could earn working add to unemployment.

Another factor keeping unemployment high in the future will be the promised increase in the federal minimum wage. Businesses are likely to accelerate the type of investments needed to mechanize as many jobs as possible, to avoid future labor costs. The lack of jobs for low-skilled workers will price many out of the market, increasing hardship among those most vulnerable.

The longer-term negative implications for the economy won’t become apparent until beyond midyear at the earliest. It’s necessary to monitor policy trends closely to determine how quickly and damaging the new policies will be.

My book Rich Nation, Poor Nation documents five times during the past century when the United States moved away from free-market classical principles. Each case involved tax increases, rapid rises in government spending and regulations, and greater government control over markets. In each case, low-income workers suffered the most.

Last year marked the end of the latest round of pro-growth economic policies. With the massive increase in money, in federal spending, and in government controls over the economy, we enter a new cycle. This will be the sixth time since 1913 we will adopt policies that move the economy away from pro-growth, free-market, classical principles. As with the previous five, the main victims will be the poor.

The false lesson our nation appears to have accepted is that we can create prosperity can by relying on the generous policies of our government.

If history is a guide—and I believe it is—the economy will do well for six to twelve months. Sometime between April and September, we will find out the extent to which President Joe Biden and the narrow Democrat majority in Congress (when including Vice President Harris as tiebreaker in the Senate) will go in adopting their agenda.

As policy changes move through Congress this year, we will be in a better position to anticipate both the timing and extent of the damage.

For now, my forecast is that the economy will begin to show signs of disappointingly slow growth and rising inflation late this year and early in 2022.

My liberal friends insist the upcoming policy moves will not do serious damage to the economy. I hope they’re right. I would be very happy to have to apologize and congratulate them on producing sound results. However, with the same agenda having failed on five previous occasions, the odds for success aren’t promising.

Money Sluices Open Wide

The Federal Reserve continues to purchase $80 billion in Treasury debt and $40 billion in mortgage-backed securities each month. As a result, the Fed is pumping $120 billion in new reserves into banks monthly.

This liquidity has been so great, banks can’t use all of it. They have left most of their new reserves on deposit with the Fed. These deposits are called excess reserves (the red line in the chart below). Excess reserves represent potential liquidity. They will turn into liquidity and money when the Fed uses their excess reserves for loans or investments.

Securities Held by the Federal Reserve and Excess Reserves

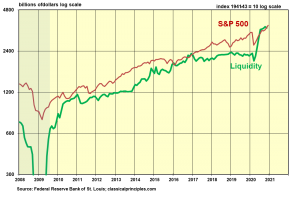

If we subtract excess reserves from total securities held, we have a measure of the net increase in reserves going into the economy. The following chart shows this measure (the green line). It also shows stock prices, since liquidity is often a key element involved in major changes in stock prices.

Liquidity & Stock Prices

Most monetary indicators confirm Fed policy is highly expansive. The only exception is yield spreads, which point to a slightly restrictive policy. The Fed’s control over interest rates is probably a factor distorting the normal reliability of yield spreads in measuring policy.

The Fed has indicated it intends to keep interest rates low and provide sufficient money to boost the economy through at least the next year. The Fed is unlikely to change its interest rate target any time soon. Even If spending and growth remain strong (as I expect), unemployment will remain higher than the Fed deems acceptable. Hence, market interest rates should remain relatively stable well into next year. Even if short-term interest rates remain low while spending accelerates, look for longer-term rates to creep up slowly, in anticipation of an increase in inflation.

On balance, the explosive increase in liquidity continues to provide a strong tailwind for both the economy and the stock market.

The State of the Economy

Amid ongoing lockdowns, a surge in COVID cases and deaths, and political turmoil, the economy has managed an amazing rebound since April of last year.

The chart below shows monthly estimates of real output (real GDP). These estimates use monthly data on wages and salaries, consumer spending, jobs, shipments, and business surveys to track the overall economy.

For example, in November, total real wages and salaries were 0.7 percent below the fourth quarter of last year. Compared to last year, real measures show consumer spending was 2½ percent below, real disposable income was 3 percent above, retail sales were 3 percent above, and payrolls were 6 percent below a year ago.

U.S. real gross domestic product increased at an annual rate of 4.0 percent in the fourth quarter of 2020, according to the advance estimate released by the U.S. Bureau of Economic Analysis on January 28. The economy’s momentum is still fairly strong, and new orders indicate the strength will continue into the spring. Unfortunately, the good times won’t last much beyond that.

")

{kind=link}

[…] State of the Economy: Near Term Good, Long Term Awful – Heartland Daily News […]