The first decade of Obamacare raises questions about the program’s lofty promises and its actual performance.

In a post on X, formerly Twitter, President Joe Biden noted that 301,000 “new customers” had signed up in the first week of the open enrollment period that began on November 1. But a study released by the Paragon Health Institute found that the health insurance marketplaces established under the Affordable Care Act (ACA) attracted half as many people as projected by the Congressional Budget Office (CBO), at three times the projected cost to taxpayers.

“The ACA’s individual market policies have produced far less enrollment at a much higher unit cost than projected, write Daniel Cruz and Greg Fann, authors of the Paragon report, titled “The Shortcomings of the ACA Exchanges: Far Less Enrollment at a Much Higher Price.”

ACA Created Federally Regulated Exchanges

Cruz and Fann, actuaries with extensive backgrounds in health care, place Obamacare in historical perspective.

“The passage of the Patient Protection and Affordable Care Act (ACA) in 2010 represented one of the most significant changes in federal health policy since the Social Security Amendments of 1965, which established Medicare and Medicaid,” Cruz and Fann write. “The principal goal of the multifaceted law was to reduce the number of uninsured Americans. The primary barrier to insurance coverage was presumed to be cost, and the intent of the law was to appropriate financial resources to provide coverage incentives for lower-income people.

“The means of accomplishing this goal were two-fold: (1) enhanced federal funding for states to expand eligibility for Medicaid and (2) restructuring the individual market into federally regulated exchanges with large subsidies linked to both premiums and household income.”

Obamacare’s Medicaid Expansion

The Paragon study confirms the decisive role the ACA’s expansion of Medicaid eligibility has played in getting people to sign up for Obamacare.

“While ACA advocates focused on the private market reforms when selling the legislation to the public, the vast majority of individuals who gained coverage following the implementation of the law have done so through Medicaid,” write Cruz and Fann. “Of the 19 million Americans with health coverage after the ACA was implemented, 17.4 million were covered under the newly eligible Medicaid expansion group.”

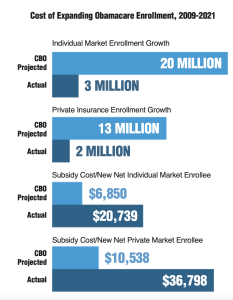

These figures are in sharp contrast to projections made by the CBO in 2013, the year before the ACA went into effect. The CBO projected a health coverage increase of approximately 25 million Americans, evenly split between new ACA exchanges and the expansion of Medicaid. This lopsided result occurred, the study says, even though ACA subsidies have increased by more than 45 percent since 2014.

(Source: Paragon Health Institute)

ACA Efficiency Under the Microscope

There has not been much research on the efficiency of the ACA, say Cruz and Fann.

“Health coverage policy efficiency is defined in terms of the increase in overall coverage relative to the taxpayer cost of achieving that increase,” write Cruz and Fann. “While ACA enrollment figures have been reported—and sometimes singularly celebrated—on growth alone, without regard to underlying cost, assessments of efficiency have been lacking and have resulted in a poor understanding of policy efficiency.

“ACA exchange spending of $60 billion in 2021 cost taxpayers $36,798 per additional private insurance enrollee ($20,739 per additional non-group enrollee), more than triple CBO’s original projections of $10,538 and $6,850, respectively. Overall, employer coverage dropped by 1.3 million, and non-group coverage increased by 2.9 million.”

Employers Cancel Health Insurance

Indeed, the study shows that since the enactment of Obamacare, employer-sponsored coverage has declined significantly, particularly among small businesses.

“According to the most recent (2022) KFF Employer Health Benefit Survey, small employers (3-199 employees) are increasingly not offering health benefits to their employees, with 51 percent offering coverage in 2022, down from 69 percent in 2010,” write Cruz and Fann. “The cost of insurance is cited as the primary reason employers are not offering coverage. Many of the ACA provisions—including benefit minimums, essential health benefit requirements, and the small group market single risk pool—have driven costs higher for these employers.”

Obamacare’s original goals have been further undermined by changes to the program since 2014, including the federal government’s cessation of reimbursing insurers for cost-sharing reductions (CSR) payments, prompting insurers to raise the price of premiums for ACA silver plans to reflect the actuarial value of those plans.

Further, say Cruz and Fann, the 2021 American Recovery Plan Act “reduced required income-based premium contributions for subsidized enrollees and expanded the population eligible for subsidies.”

“Meanwhile, unsubsidized middle- and upper-class families are forced to pay the full cost of plans and have limited options outside of the individual ACA market, resulting in minimal overall non-group enrollment gains due to the ACA,” write Cruz and Fann.

Obamacare Not a Success

“This study should silence all claims that the ACA has been a success,” said Dean Clancy, a senior health policy fellow at Americans for Prosperity. “The law has failed to deliver more affordable care to people and transferred hundreds of billions of dollars from taxpayers to insurance companies—all while, remarkably, making it harder to access quality care.”

“To improve government, it is vital that we analyze how public programs actually work,” said Brian Blase, president of the Paragon Health Institute. “A fair analysis of the ACA finds that it has largely been an expansion of the Medicaid welfare program and that the individual market is in poor condition, with most enrollees needing to receive giant subsidies to purchase coverage.”

Bonner Russell Cohen, Ph. D. (bcohen@nationalcenter.org) is a senior fellow at the National Center for Public Policy Research.

")

{kind=link}